Margill Loan Manager – Ageing report – with refinanced loans

Q: If a loan was refinanced and the payments revised based on the refinanced balance, can the loan account still be in arrears? Doesn’t the refinancing and revised payments take into consideration any prior arrears?

A: Arrears are always a little tricky with refinanced outstanding amounts since a human must take a decision as to whether the new payments to be added are simply extra payments or are to compensate for the unpaid payments in the past. The examples will help…

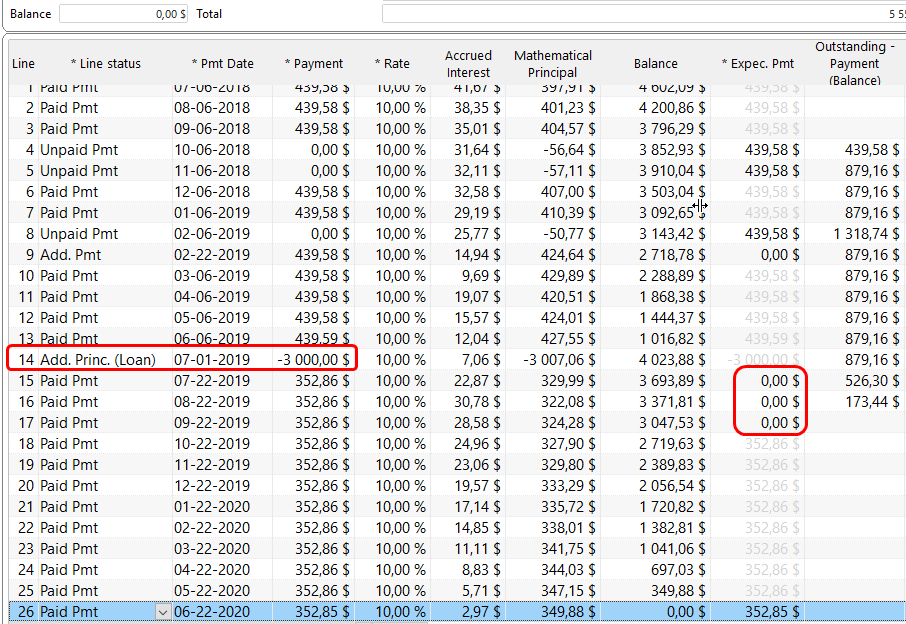

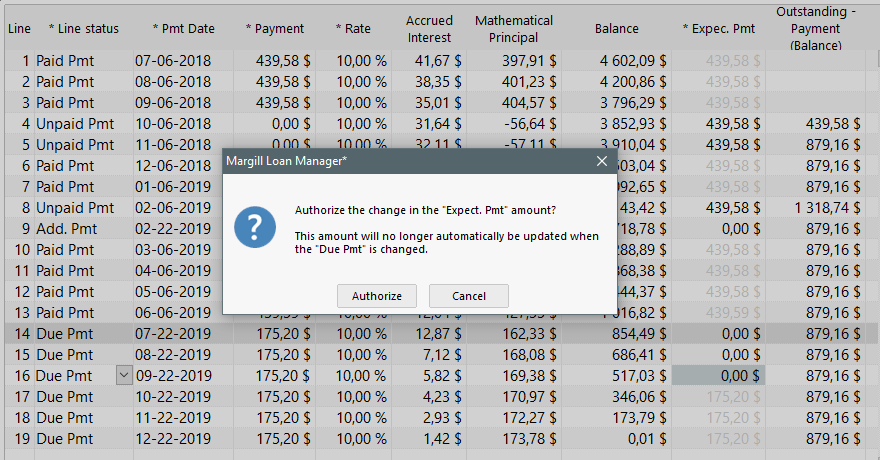

A most important column in the schedule is the “Expected Pmt” column. This column indicates how much was expected for this line and subtracts the actual payment amount from this amount to generate the Outstanding amount.

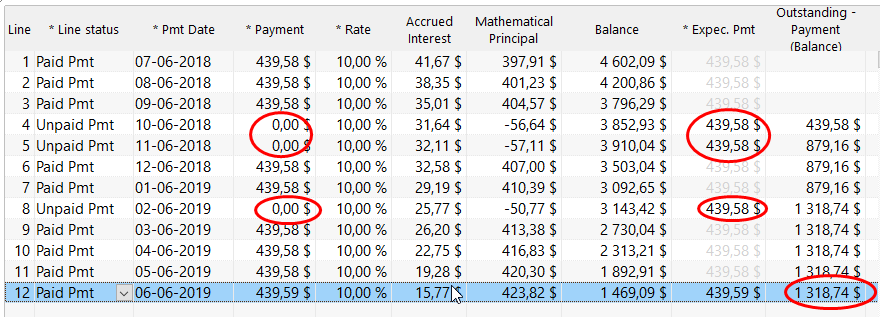

- On 07-06-2018 I was expecting 439.58 and got a 439.58 payment so Outstanding = 0.00.

- On 10-06-2018 I was expecting 439.58 and got 0.00 so Outstanding = 439.58 and so forth

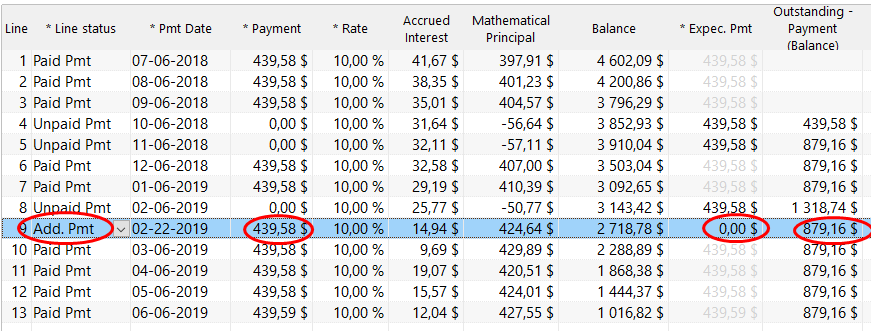

If an extra payment (unexpected in the normal scheme of things) is made, then the Expected Pmt should be 0.00 and the Outstanding is thus reduced.

If a loan is refinanced, you must make sure that as of this moment, your Outstanding amount gets progressively reduced to 0.00 and you do this with the Expected Pmt column in which you would put the Expected Pmt to 0.00 for the new payments that are added or changed to give 0.

In the above example, the loan is refinanced with lower payment amounts since the 439 was too high for the borrower – 6 payments were added and these now become 175.20 to reach 0.00. One could argue that these payments are extra and thus the Expec. Pmt should be 0.00 for each, so we manually change the Expect. Pmt to 0.00.

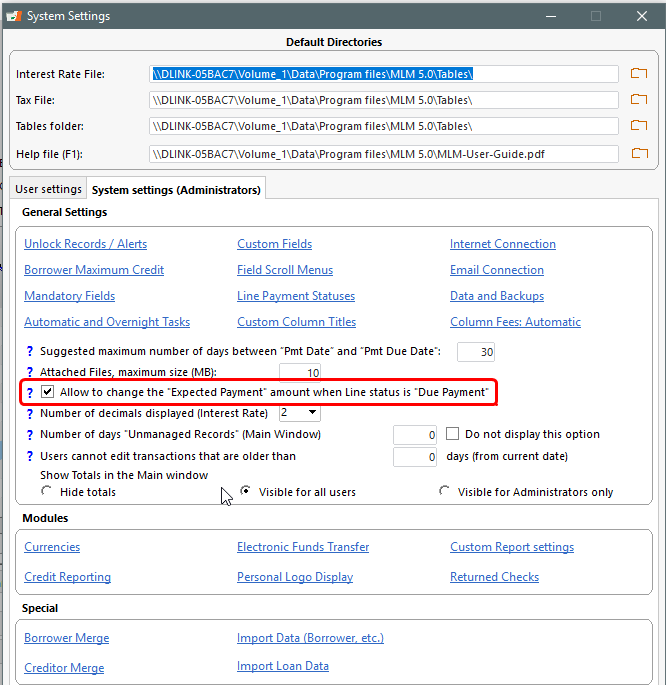

NOTE: In order to be allowed, to change the Expected Pmt amount, this must be allowed by the Margill Administrator in Settings:

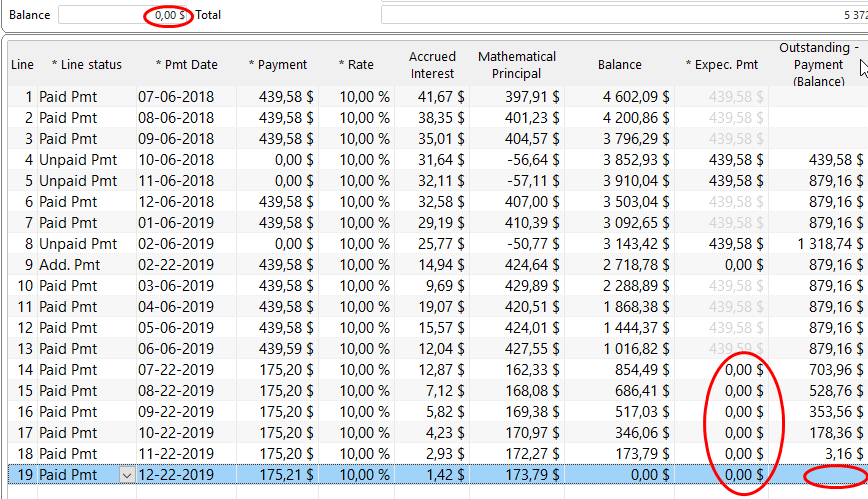

As these new payment become paid over time, the Outstanding amount gets reduced…

If on the other hand, a second amount (new Advance) was lent to the borrower and extra payments were added, then I would not change my Expected Pmts to 0.00 since these new payments become part of the normal payments, in the normal scheme of things. So Outstanding is quite subject to interpretation…

I actually cheated below by entering 3 of the 12 new payments with Expected Pmt of 0.00 to bring my Outstanding back to 0.00. Outstanding must be 0.00 or greater, never less than 0.00 even if one could argue the borrower overpaid.