Intercompany Loan Management with a Loan Servicing Software

Intercompany loans

Very often, when a company has many subsidiaries, branches or franchises, the head office will afford loans to these other entities. These subsidiaries in turn can lend to other entities and so forth. These intercompany loans often represent quite a challenge to the accountants and controllers since the loans are not part of the company’s core business and are most often very different from run-of-the-mill personal loans and mortgages.

The challenge of intercompany loan administration stems from multiple factors:

- These loans are often irregular with sporadic payments that are not due at set dates as in regular loans.

- They can also be interest-only, fixed-principal, principal-only, and of course, principal and interest (P&I).

- They often include irregular capital advances, so are somewhat like lines of credit adding yet another level of complexity that most loans servicing platforms cannot handle.

- Changing or variable interest rates are another challenge faced by the parent company. Often the interest rate will be x basis points above or below central bank rates or LIBOR rates (Overnight, 1 week, 3 months, etc.). Updating loans as the rates change can be a time consuming task where errors are easily made.

- In some situations, there are multiple entities involved in the same loan: multiple creditors (participating loans) and even multiple borrowers (co-borrowers) for these loans. Each has a stake as a percentage of the total loan amount or dollar amount.

- We have seen many examples where the borrower pays back more than the principal, so the lender actually becomes the borrower. The lender now owes the borrower. So negative interest is actually calculated. The roles can change regularly as the lender provides new capital advances and as the borrower pays back…

- Multinational organizations often have loans in multiple currencies.

If the people responsible for setting up loans and payment schedules are not from the banking sector, the calculation method specified in the loan agreement may not have been followed or is simply guessed based on the calculation and loan servicing tools available. This in turn may not correspond to the parties’ true contractual intent.

- Some loans in a lender’s portfolio may use one method (Simple interest) while other loans use Compound interest. Even in Compound interest, two methods are commonly seen: the Banking or Effective Rate method that uses a special formula with an exponential component; and what we term Simple Interest Capitalized where simple interest is used to calculate interest on a daily basis. And if interest is not paid at the end of the month (for monthly compounding) then the new balance (taking into account the unpaid interest portion) now generates interest. The US government often uses this method.

- The compounding frequency (annually, semi-annually, monthly, daily, etc.) must also be factored in.

- Finally, the Day count (so number of days to be used in the calculation – 365, leap year 366 and 360) may vary from loan to loan or may not even have been considered.

Since these lenders and borrowers are not professional lenders, the companies are often ill equipped to deal with these loans. Spreadsheets are the most common solution. Excel does a great job for a few loans but when the volume increases, the spreadsheets become practically unmanageable! Exceptions are simply ignored, interest improperly calculated, etc.

Our Loan Servicing Software, Margill Loan Manager offers a solution for all these problems with the capacity to easily:

- Create regular payment schedules

- Create irregular payment schedules

- Add principal advances (additional principal to a loan)

- Compute interest-only payments

- Compute principal-only payments

- Compute fixed-principal payments

- Add automatic fees for late or missed payments (although this is less common in intercompany loans)

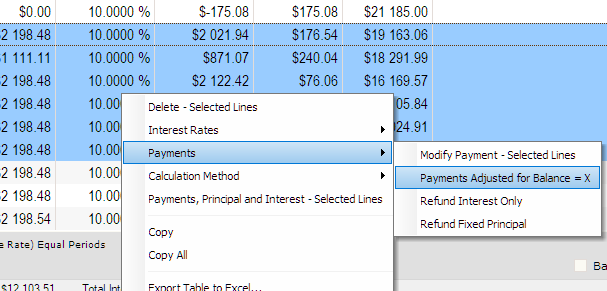

- Create schedules using historical variable interest rates

- Increase or decrease the interest rates for one or multiple loans (in batches) based on the rate type and the new interest rate (LIBOR, Base rates, etc.)

- Include multiple entities as creditors (holding company, bank, subsidiary) and multiple entities as borrowers, co-borrowers and guarantors

- Create Participation loans (percentage ownership for creditors and for co-borrowers)

- Include not only intercompany and bank loans, but also distinguish these from unrelated third-party loans

- Allow a loan to eventually yield a negative balance with interest computed on this negative balance. The rate could even be changed or set to 0.00% when the loan becomes negative

- Create loans in various currencies, and then convert these currencies back to a unique currency based on the desired exchange rate

- When monthly or even daily transaction volumes become important, a very simple Excel file can be used to enter new payments or advances or to post set due payments directly to Margill

- Electronic Funds Transfers (EFT) (ACH) directly in Margill (US and Canada)

- Extract, in seconds, borrowing activity, P&I balances, accrued interest, paid interest, etc., for the whole loan portfolio or a part of it

- Produce the accounting Debit and Credit report which can then be imported to the company’s General Ledger (GL) in QuickBooks and Sage. The report can also be exported to generic formats: Excel, CSV and TXT

See also our White Paper on Interest calculations: https://www.margill.com/en/interest-calculation-white-paper/

You can also try our software for 30 days for free: https://www.margill.com/en/margill-loan-manager-free-trial/

Or Schedule a demo: https://www.margill.com/en/schedule-a-demo/

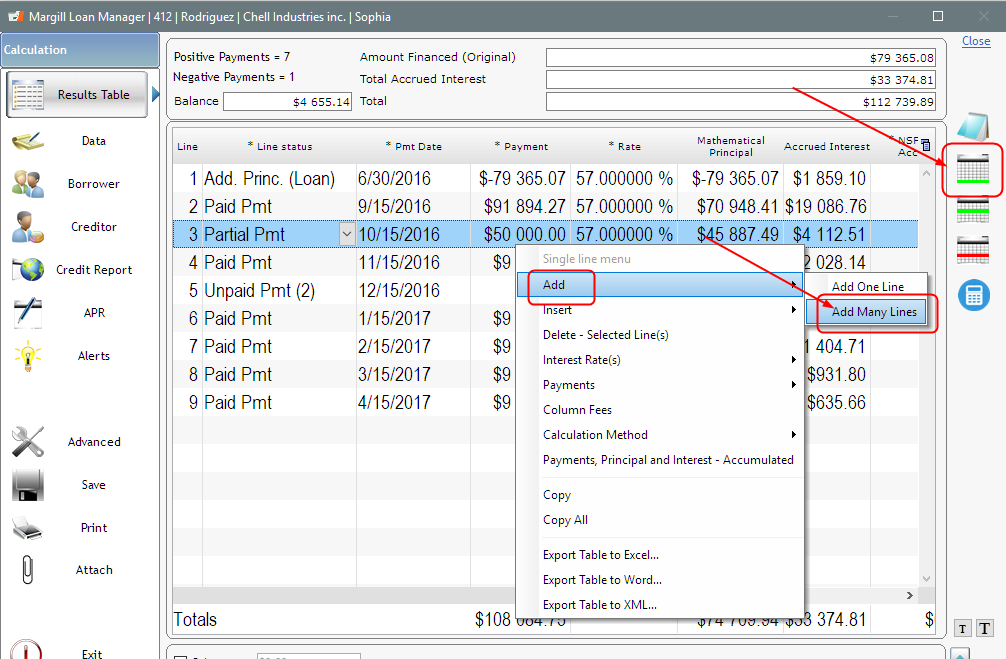

icon to the right of the window or right click with the mouse > Add > Add Many Lines.

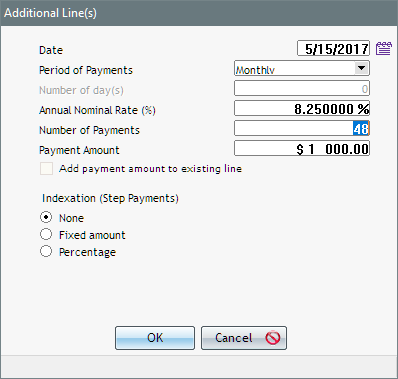

icon to the right of the window or right click with the mouse > Add > Add Many Lines.