Margill Loan Manager version 4.2 webinar

We did a Margill Loan Manager webinar back in December regarding version 4.2

If you missed it, or you would like to see its content, you can refer to the following video and document:

We did a Margill Loan Manager webinar back in December regarding version 4.2

If you missed it, or you would like to see its content, you can refer to the following video and document:

To all Margill Law Interest Calculator users, we have updated the 4.56.110(3)(b) interest rate table to correct the error discovered.

In March 2017, while reporting the Historical Judgement Rates to the Office of the Code Reviser, they discovered an error in the rate from February 2016 through March 2017.

If you want the latest version, please update your interest tables.

The Margill Team

Questions:

1. In terms of the accounting report and accounting identifiers, are these captured at the borrower level, or the record level? How is this selection made and where is it used/displayed on the accounting report?

2. In our accounts we split interest accrued and other fees by product type, i.e. a separate GL account by product, is it possible to do this in the accounting report or would we need select and run it for each product type?

Answers:

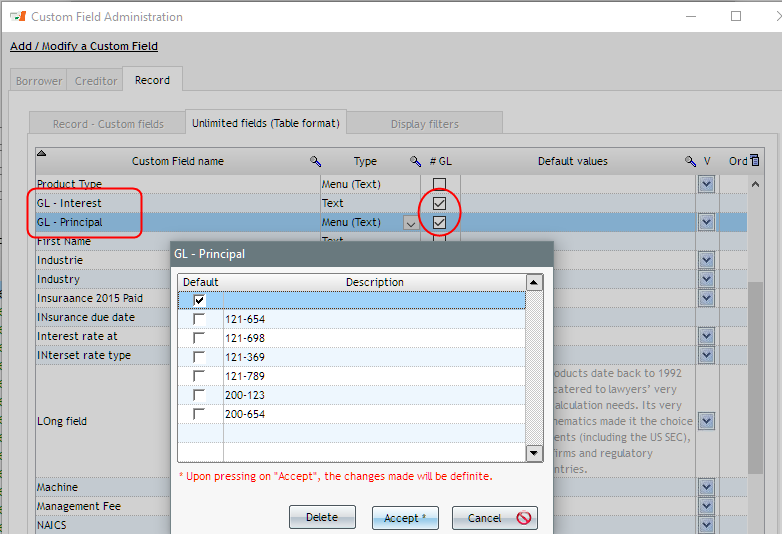

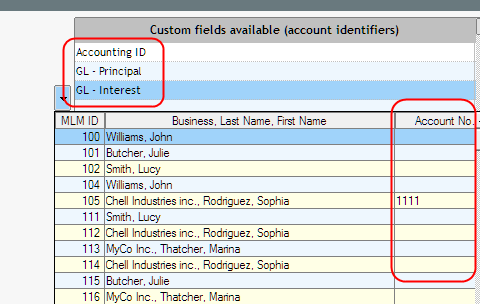

1. You can have as many General Ledger (GL) accounts as you want in Margill and report for each. These can be assigned to the Loan (Record), the Borrower and/or the Creditor.

These can be included as Custom fields by checking the “#GL” column. You can even create a scroll menu if there aren’t hundreds of these.

You can populate these very quickly with the Global changes (select Records in the Main window, right click with the mouse).

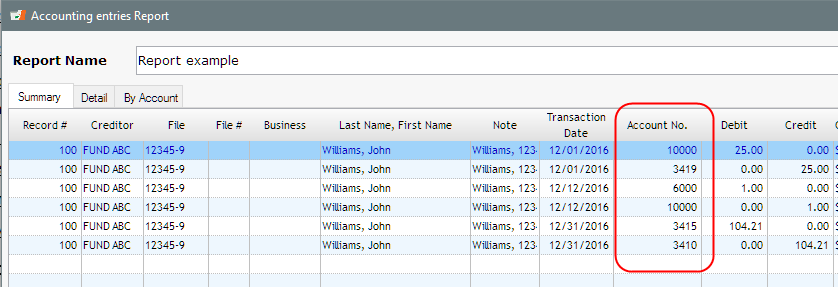

The GL accounts created are then used in the Accounting Entries report (only one Record has an account below…).

When you run the report, the GL number will show up here:

This detail can then be exported to Sage, QuickBooks, Excel, CSV, TXT. Or you can get a summary – “By Account” tab.

2. Yes you can have a GL account by product type. If each Record (or loan) is for one product type, then you would create a scroll menu for the GL by product type and assign to each Record individually. You can then run one report with all your records and the proper GL number will be assigned for each debit and credit.

Question:

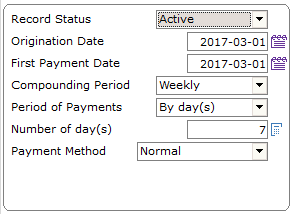

How to setup weekly or biweekly payments in Margill Loan Manager?

Answer:

When creating a new record, set up the Period of Payments at ”By day(s)” and input 7 for weekly or 14 for biweekly payments.

We also suggest that you setup the Compounding Period to match the Period of Payments.

Consult the new User Guide for the Margill Loan Manager – Version 4.3 here.

We already mention on our website that we sell in 38 countries, but it is always interesting to see our software at work overseas.

Its flexibility and powerful mathematics make our Loan Servicing Software useful for our new client in South Africa, Forward Finance.

Welcome from the Margill team!

For more testimonials: https://www.margill.com/en/client-testimonials/

Questions:

Question:

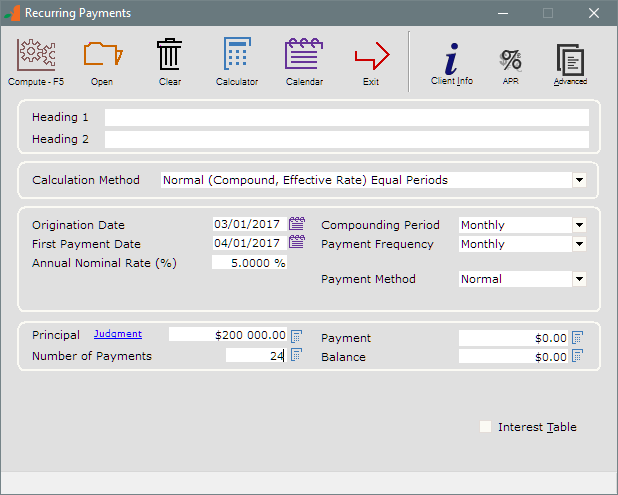

I have a principal of $200,000 starting 03/01/2017 (over 24 months) and the last payment to be made on March 1, 2019.

First payment is on 4/1/2017 at unknown amount.

Two $50,000 lump sum payments to be made on 05/01/2017 and 05/01/2018.

I must also compute the payments in between the $50,000 payments.

Interest at 5 percent.

Can did this be calculated in one calculation?

Answer:

Yes. Pretty easy to do in fact.

Go to “Recurring Payments” caclulation.

I will suppose compounding is Monthy.

Enter this preliminary data

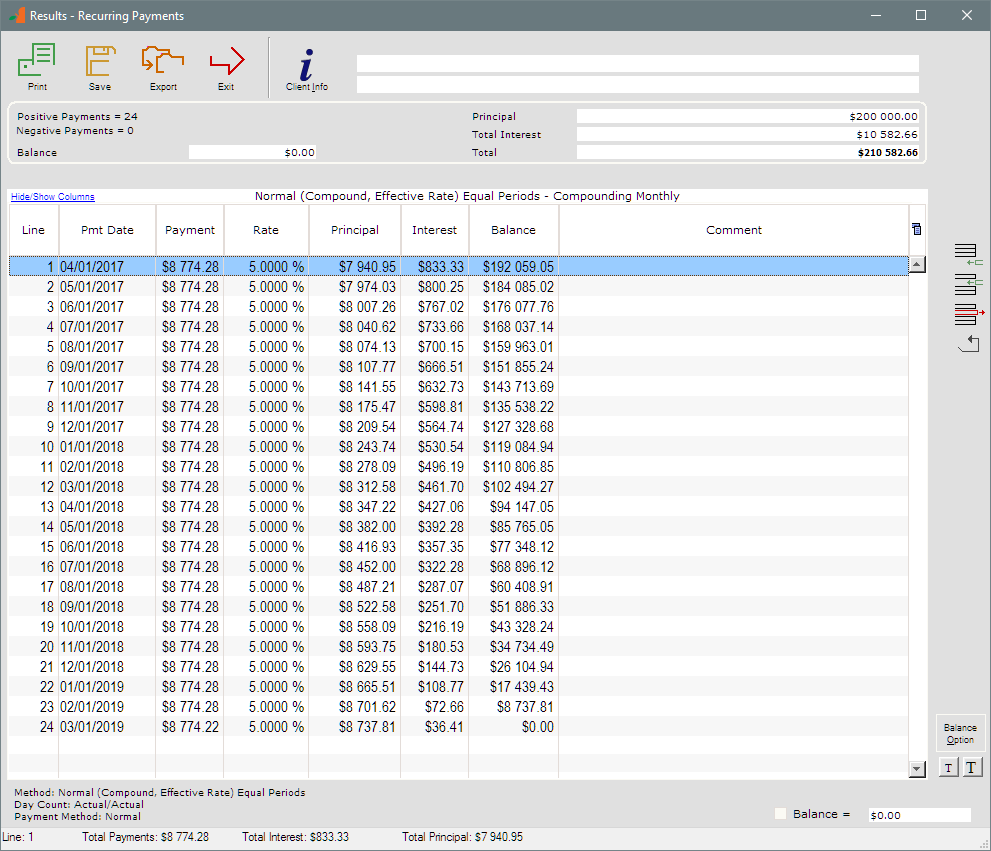

Compute or F5 to get these preliminary results:

You can totally adapt this to your needs.

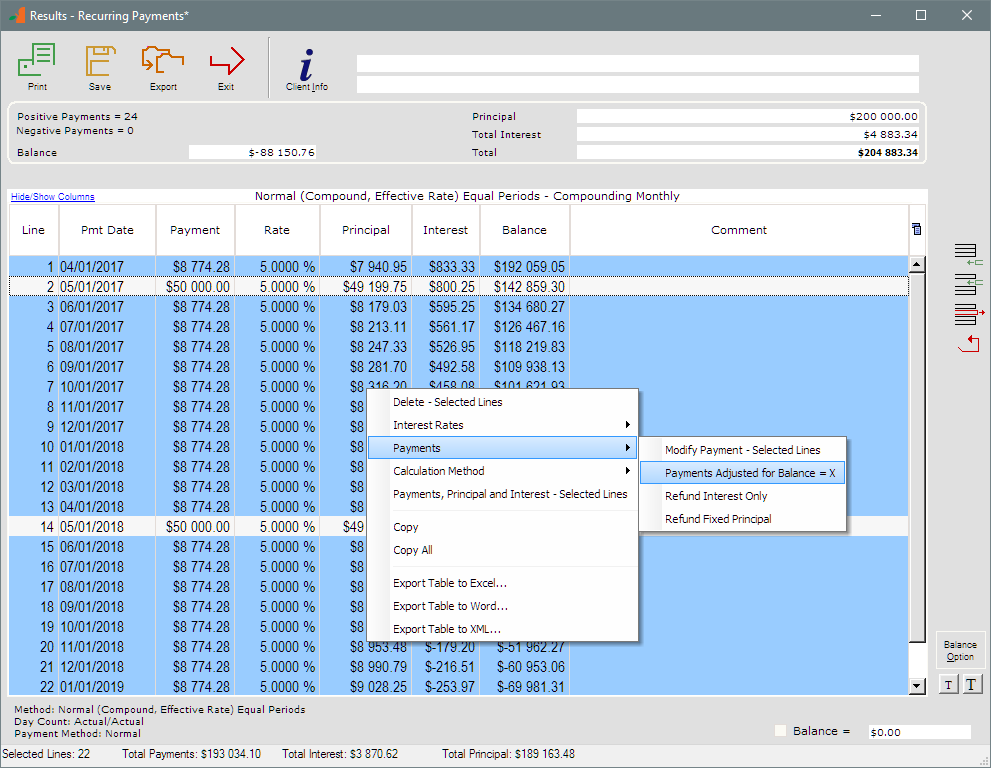

We know payments of 50,000 are to be paid on 05/01/2017 and 05/01/2018. Change these directly in the schedule.

As for the payments in between, they must be recomputed so as to reach a balance of 0.00 at the end.

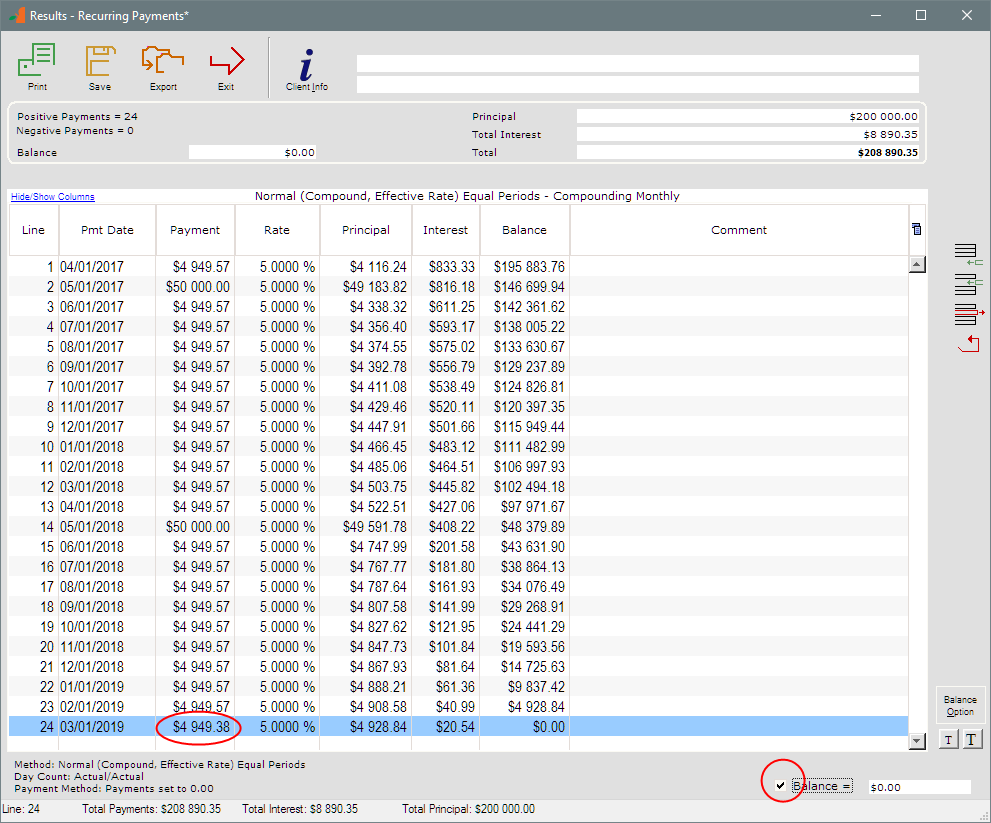

Select all lines (Ctrl A) then exclude the 50,000 lines (Ctrl click on lines 2 and 14) and right click with the mouse. I want my balance to be 0.00.

And here you have it. My last payment if off by a few cents so I checked “Balance = 0.00” on the bottom right.

Save that calculation and you can then adapt to what happens for real over time.

Took less than a minute….

Client comment after post:

Marc, I just checked it. You made four people very happy today. One client, two attorneys, and me.

I really appreciate your availability, patience, and instruction.

Question

How can we obtain the loan-to-value (LTV) in Margill Loan Manager? Read more